****Please for the love of your chosen deity this is for writing and educational purposes only- I know its tempting but do not try any of this at home!!!****

Medical ether and industrial ether are basically the same.

Medical oxygen and industrial oxygen are also basically the same (industrial oxygen for welding is actually more pure than medical oxygen, but this doesn’t matter much).

Most drugs are completely effective (>90% of expected active drug) for at least 5 years after their “expiration” dates provided they are kept in their original, unopened packaging. Some drugs are completely effective for decades if kept in controlled conditions.

According to one study, that fact includes EpiPens.

In patients who have never chronically used opioids, a combination of 1,000mg acetaminophen (tylenol, paracetamol) and 400mg ibuprofen (motrin, advil) every 6 hours have been shown to be equivalent to the

standard starting dose of oxycodone/hydrocodone in treating acute musculoskeletal (breaks, strains, sprains, dislocations) pain.

Rotating these medications (giving the acetaminophen, waiting three hours, giving the ibuprofen, waiting 3 hours, giving the acetaminophen again, and so on) makes them more effective. This works pretty well any time you have more than 1 medication for the same thing.

Benadryl can be used as a local anesthetic if you can find (or make) a form of it that can be safely injected.

Nitrous oxide cartridges for artisan whipped cream dispensers (naturally found in an abandoned Starbucks in the aftermath of an apocalypse, or on Amazon) can provide up to 3 minutes of decent conscious anesthesia each (they need to be emptied into a whipped cream dispenser and given with 25-50% regular air or oxygen and breathed in order to work well).

Wound-wise, you don’t need saline or sterile water to clean an already dirty wound. If you would drink it, its safe for wound cleaning.

Speaking of that, you can make an irrigation syringe by poking a small hole in the top of a pop bottle filled with irrigation fluid (or tap water).

Many venoms can be at least partially degraded by soaking the bite site in very hot water.

You can make a spacer for an albuterol inhaler out of a 16oz pop bottle by cutting a hole in the bottom, placing the inhaler through it (with some space around it for air to get in), and breathing through the top.

A pressure cooker (stovetop or electronic) is basically just an autoclave re-purposed for food. Throw a shelf in there to sit over a small amount of water and you can quickly sterilize temperature/pressure resistant equipment like metal scalpels.

If you get the balance right, you can centrifuge something/blood with a hand drill by attaching a test tube to each side of the spinny part.

It seems counterintuitive because generally bacteria eat sugar, but raw honey works as well or better than most antibiotics when preventing/treating wound infection (the honey goes in the wound, btw, but eating it would still taste good).

Regular insulin does not actually need to be refrigerated unless its being stored for long periods. Even open, it will still last about a month at room temperature without significantly degrading.

IV is not the only form of rehydration. Oral rehydration is actually best, but you can infiltrate sterile IV fluids slowly into fat, or provide a very slow enema of tap water or even slightly brackish water that the body will absorb and utilize.

Smelling isopropyl alcohol or peppermint oil can help with nausea.

Fishing line is extremely similar to suture material. Dental floss is less so.

You could, theoretically, hook up as many as 4 people to the same ventilator as long as they all had relatively similar ventilation needs and they were all chemically paralyzed to the point where assist-control mode would be appropriate. Programmed tidal volume would be the total of all four patients.

You can re-locate a dislocated shoulder by having the person lay face down with the dislocated arm hanging off the side. Tie about 10-15lbs to it and let the weight slowly release the muscle and reduce the shoulder.

Most of these came from the book Improvised Medicine: Providing Care in Extreme Environments, By Kenneth V. Iserson.

Here’s another exciting round of “I hope the internet doesn’t blow up”! Rumor has it that you use the language of MONEY you might get people’s attention faster, so here goes nothing…

(You can use my template (3rd image) if you want, just swap out the name and state and whatever else applies to your business model. Make it personal!)

pretty much yeah

my personal bullet points:

I run a small business online

removing net neutrality will limit my customer base

liming my customer base is a great way to kill my business

you don’t want to kill small businesses do you

also maybe worth mentioning: Portugal already did this. We / America can do better. (Patriotism etc.)

That’s what is going to happen if we let Ajit Pai, the FCC chairman, go through with repealing Title II (AKA Net Neutrality).

Simply put, without Net Neutrality, Internet Service Providers like Comcast, Verizon, and AT&T will be able to “bundle” websites much like cable ON TOP OF paying for internet connection. “Want access to Netflix AND Tumblr? Get the Entertainment Package! $40 a month. What about Amazon and Ebay? Add an extra $20 a month to get the Shopping Package.”

Not only will they be able to bundle websites and charge more, they will also be able to censor and block websites that they don’t agree with entirely.

THIS WILL BE THE END OF INTERNET AS WE KNOW IT.

For business owners, it will be even worse. Ex: Comcast will ask Amazon to pay high fees to be available in a low-cost package, fees that websites like Poshmark or Etsy will not be able to pay. Therefore, only Fortune 500’s will be available to web users at a low cost. Say goodbye to Etsy (unless you’re willing to shell out $70 a month for the “All-Inclusive” package).

To learn about Net Neutrality, why it’s important, and/or want tools to help you fight for Net Neutrality, visit BattleForTheNet (https://www.battleforthenet.com)

There are five people deciding the future of the internet, three men (Rep) and two women (Dem). The two women have come out as No votes. We need only to convince ONE of the other members to flip to a NO vote to save Net Neutrality.

There are many ways you can help:

WHAT TO DO IF YOU’RE A LAZY TUMBLR USER WITH ANXIETY WHO TRIES TO HELP WITH JUST REBLOGS / LIKES:

Here are 2 petitions to sign, one international and one exclusively US.

(After you sign make sure to verify via email, it may take up to 30 mins to receive the email).

Text “resist” to 504-09. It’s a bot that will send a formal email, fax, and letter to your representatives. It also finds your representatives for you. All you have to do is text it and it holds your hand the whole way.

HERE ARE MORE STRAIGHTFORWARD ACTIONS YOU CAN TAKE:

These are the emails of the 5 people on the FCC roster.

Blow up their inboxes!

Ajit Pai – Ajit.Pai@fcc.gov

Mignon Clyburn – Mignon.Clyburn@fcc.gov

Michael O’Rielly – Mike.O’Rielly@fcc.gov

Brendan Carr – Brendan.Carr@fcc.gov

Jessica Rosenworcel – Jessica.Rosenworcel@fcc.gov

You can support groups like the Electronic Frontier Foundation and the ACLU and Free Press who are fighting to keep Net Neutrality:

Most importantly, VOTE. This should not be something that is so clearly split between the political parties as it affects all Americans, but unfortunately it is.

so it’s open enrollment time, which means you need to pick a health insurance plan from the exchanges! it can be daunting as shit, for sure, especially if you don’t live in the filthy weeds that are the business side of our garbage health care industry like yours truly does.

so! here’s a quick rundown of some of the vocabulary:

premiums: this is what you pay per month for the glorious honor of having insurance coverage. it does not count towards your deductible or out of pocket maximum. depending on your income, you may be eligible for a subsidy or other financial assistance to make your premiums more affordable.

deductible: this is how much in health care costs you have to pay before your insurance starts really kicking in. for example, my insurance through work had a $1,500 deductible, so the copays and coinsurances and lab costs that i had to pay early in the year, before i had another surgery, were fully my responsibility until i’d paid out $1,500; after that, my insurance started covering a flat 80% of everything, including copays. basically, the deductible is how many actual dollars you have to pay out for medical costs before your insurance takes over.

if you’re someone who goes to the doctor a lot, like me, you’re probably going to want a plan with a lower deductible, which will have a higher premium; however, in the long run, you’ll come out more ahead with a high premium/lower deductible.

on the flip side, if you’re generally healthy and just need an annual checkup, flu shot, ob-gyn annual, etc., then you probably want a lower premium/higher deductible plan.

out of pocket maximum: this is the cap on how much– aside from premiums– you should have to pay in health care costs in a year. most plans on the exchanges right now have a high deductible and higher OOP max.

network: this is the collection of providers (doctors, surgeons, urgent care facilities, imaging facilities, etc.– any clinical medical care or medical service provider) that are contracted with the insurance plan. this means that they have an agreement with the plan to accept payment from that plan for services. you can still see out of network providers, but your plan may have a separate out of network deductible that is higher and that you pay separately from your main deductible (for example, if your plan deductible if $5,000, you might have a separate out of network deductible of $5,500; even if you’ve already paid of $4,950 of your regular deductible, if you see an out of network doctor, you’re going to have to hit the $5,500 deductible in copays and whatnot before the insurance covers them fully).

most insurers have their own website that identifies what doctors are in network. sometimes you can access this without being on the plan already, sometimes you can’t. a decent, though inconsistent, workaround is to use zocdoc, where you can put in the plan type you’re thinking about switching to and see what doctors are in network. the drawback to zocdoc is that contract status is doctor-reported, so if the doctor’s office in question is slow to update, the records may be out of date.

another option to determine network availability for a specific doctor or care group is, if you’re okay hopping on the phone, to just give them a call and ask outright if they’re going to be in network for plan ___ in 2018.

if you’re like me and hate talking on the phone, the other option is that large provider groups, and a good number of smaller groups and individual providers, will often also have accepted insurances on their websites. in my experience almost all providers who have privileges at a hospital will have that listed on their pages on the hospital’s website.

copay: this is a flat fee you pay to a provider when you see them. it’s like the cover charge at a bar: you pay $20 to get in the door, and then you get the dubious honor of also paying for the drinks and food you buy inside on top of that.

coinsurance: this is a percentage charge for seeing a provider. instead of a $20 copay for the cost of the visit to see doctor bob, you’re charged, say, 10% of the total cost of all charges associated with you visit to see doctor bob. if you don’t get much done, this may only like $10; if you get a full metabolic panel run and a bunch of xrays, it might be $100.

and the plan types:

hmo: health management organization. the concept of this plan is that you have a pcp (primary care provider – your regular doctor) who functions as your primary point of contact for all medical care. if you want to see a non-pcp doctor, you have to first see your pcp, who will write you a referral to see said specialist. specialists include orthopedists, physical therapists, neurologists, ob-gyns, etc. – any provider who isn’t your pcp, basically.

hmos tend to be cheaper for you, the beneficiary

this is because of how they’re paid out: pcp doctors receive a capitation (aka, a set flat amount) payment from the insurer for each beneficiary (you) who has them as a pcp.

so, if i’m a primary care doc and i have 200 blue cross hmo patients and i get $100 per patient, i get $20,000 from blue cross, ostensibly for the cost of care provided, but the provider keeps all $20,000 even if they only end up incurring $15,000 in costs. the downside of this for you as a patient is that this encourages pcps to get a lot of people to sign up as their patients, and then to see them as little as possible/push them out to specialists for actual care, as this lowers their costs and increases their revenues.

you may end up feeling like you’re going in circles trying to get actual care because you’re getting pushed from one doctor to another.

note: hmo plans sometimes do not cover out of network providers at all.

ppo: preferred provider organization. this plan is a free for all: if they’re in network, you can go to whomever you want. they tend to be a bit pricier (almost always on premiums, 50/50 on deductibles) than hmo plans, but you’re basically paying for ease of access. you can make an appointment directly with any specialist you so choose. these plans are ideal for people like me, since i have to see orthopedists and hematologists and physical therapists pretty regularly, and going through a pcp for each of those would be a pain.

you’ll tend to have relatively low copays within the network and higher ones outside of it

unlike some hmo plans, most ppo plans will provide coverage for out of network providers, just at a less favorable rate

epo: exclusive provider organization. this is the bastard child of the hmo and ppo and is also an increasingly common option on most of the exchanges. like a ppo, no pcp or referrals are provided; however, the network tends to be narrower and you have less choice of in-network providers and, crucially, they don’t tend to cover any out of network providers except for emergencies

important note: the classification of “emergency” isn’t just “emergency situation”, but generally is limited to a proven medical emergency in which you go to an actual emergency room or emergency department.

insurers will frequently challenge ER/ED bills to confirm medical necessity because–

in their defense, since they’re meant to cover almost the entirety of emergency bills and also because one of the quantifiable measures of success in moving to value-based care that the ACA established is lowering avoidable ER/ED admissions

–they don’t want to encourage people to go the ER/ED for just anything

high deductible/catastrophic: these are exactly what they sound like– plans for healthy young people who are pretty much only going to wind up with medical costs if something terrible and, well, catastrophic, like a car accident, happens. they have low premiums and very high deductibles (often approaching ~$10,000). these are only available to people under the age of thirty, because clearly as soon as you turn thirty you must turn into a total drain on all healthcare resources 😐

so what does all of this boil down to for you and your enrollment?

start by figuring out what financial help you’re eligible for! the exchanges generally have an option at the front end of the process for you to identify your annual income and number of dependents on your plan. this will let you know if you’re eligible for a subsidy or other financial help, and, if so, how much; you should also have an option when searching through plans on the exchanges to input estimated financial help, which will adjust the premiums in the search engine.

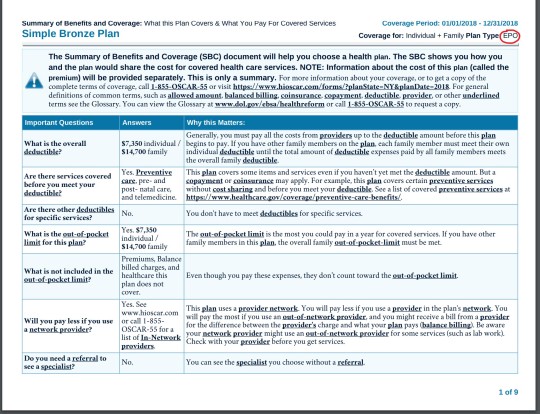

after that, start digging into the individual plan options. every exchange plan should provide a summary of benefits and coverage. it’ll be a pdf and will look like this:

that red circle in the top right there? that’s where you can identify what type of plan you’re looking at. the first page in the summary of benefits will always look the same– it’s the basic overview of the costs and definitions.

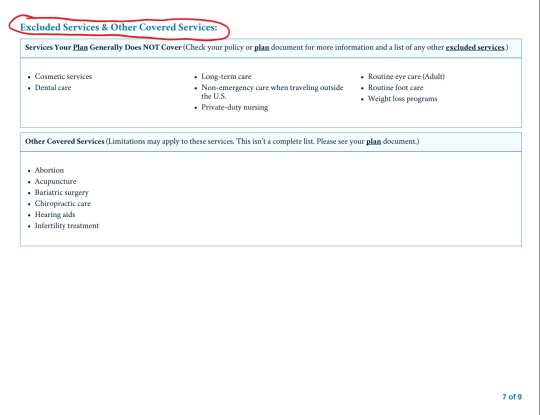

this document will also list excluded services. it’ll generally be somewhere in the middle/back half of the document and will have a clear header like this:

for me, this is the first thing i look for after verifying premium and deductible amounts. as the above picture indicates, you can find more information in the plan documents. these aren’t always directly linked to on the exchange website, but you can generally find them on the insurance providers website. these will be a lot more detailed and can be anywhere between twenty and 200 pages. ctrl + f your heart out: as frustrating and complicated as insurers can be, they can’t actually fail to disclose if they, for example, don’t cover all forms of contraceptives. they’ll disclose it in the plan documents, even if they don’t, unfortunately, have to be clear and up front about it.

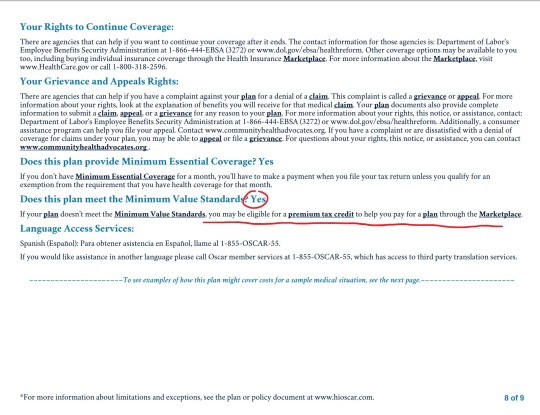

NOTE: MINIMUM VALUE STANDARDS

towards the end of the summary of benefits document will be a page that looks like this:

minimum value standards roughs out to basically meaning that at least 60% of all medical charges are covered. if the plan you’re on does not meet minimum value standards, you might be able to get a tax credit to help you buy another marketplace plan. always check for this verification when you’re researching plans.

what does all of this shit mean?

it means start here and then find your state’s exchange from there. the garbage carrot in chief established “maintenance times” on this website throughout the open enrollment period (sunday afternoons, i believe), so schedule around that. sit down on a monday or wednesday or saturday with some snacks and a cup of your favorite beer/wine/tea/whathaveyou and crank up some good music to jam to and do some research:

start with figuring out what you can afford monthly and if something terrible happens and you have to cover ER and/or surgery bills

if you have a specific doctor you want to stay with, figure out which insurances they’ll be accepting

check for coverage info in the summary of benefits documents and, if you want more detail, in the plan documents

narrow it down to a few and compare the prices

take a break and have a cookie, you deserve it at this point

pick a plan! if you’re not feeling super certain about it, go for a walk, do some laundry, pet your cat– just take a break, walk away, come back to it with fresh eyes. this is a big deal, so you don’t want to wear your brain out and give yourself a headache and then just pick one at random because you have eye strain and want to be done. open enrollment goes until december 15, so don’t rush yourself.

sign up for your plan

have another cookie and pat yourself on the back, because you just signed up for health insurance for 2018!

now take a nap because that was fucking exhausting and you deserve it

if i don’t know the answer, i can point you towards someone or some resource that will. don’t be afraid to ask me or anyone else for help! this is a complicated situation and even though the current administration is trying really hard to make it worse, there are still always resources available to you for help and guidance. all you have to do is ask 🙂

If anyone needs any help please ask me! I am a tax professional and can translate what might be confusing.

If someone says something that you only partially understand:

DON’T ask for clarification with a generic “What?” or “I’m sorry?” (In my experience, people will repeat the phrase the exact same way without helping you to understand).

Example:

Them: “Hey, do you like pahganabasa?”

Autistic Person: “What?”

Them: “Do you like pahganabasa?”

Autistic Person: “I’m sorry, what?”

Them (annoyed): “Do you like pahganabasa?”

Instead, DO repeat the part that you did understand, and substitute a “What?” for the unintelligable part.

Example:

Them: “Hey, do you like pahganabasa?”

Autistic Person: “Do I like what?”

Them: “Pineapple pizza?”

Autistic Person: (Understands the words!)

I’ve also had successes with “I’m sorry, I only heard the first half of that sentence,” or actually verbalizing my interpretation of the part I heard incorrectly as a question: “Pahgana… basa?”.

Sometimes that makes the speaker think that they might be mumbling, or verbalizing in a way that makes them difficult to understand (because there are times it’s really not your brain–it’s their mouth).

This is also a lifesaver if you have Auditory Processing Disorder. It stopped the amount of annoyed sighs because ppl thought I was deliberately ignoring them or them saying the same thing but louder (which does not help when volume isn’t the problem)

I do this a lot- I have really shit auditory processing and ADHD, and we often get sensory issues. I have to be on the phone a lot for work and my auditory processing isn’t good enough for me to really deal with phones. I’ve def done the repeating thing a lot.

Customer: “Do you have the green car with the akj;ldfjksal;fjda?” Me: “The green car with… the flux capacitor or the mobile pizza oven?” Customer: “The pizza oven!” Me: “Okay cool! Yeah, we’ve got that, and in lime green too!”

Makes my life a zillion percent easier, especially since phones add an even worse layer of difficulty to my words-to-brain lag time.

For artists who have problems with perspective (furniture etc.) in indoor scenes like me – there’s an online programm called roomsketcher where you can design a house/roon and snap pictures of it using different perspectives.

It’s got an almost endless range of furniture, doors, windows, stairs etc and is easy to use. In addition to that, you don’t have to install anything and if you create an account (which is free) you can save and return to your houses.

Examples (all done by me):

Here’s an example for how you can use it

Great find, thanks!

OMG HEAVEN!!

Bless you!!!!

@destatree we can finally design the boys apartment!!!!!

if your stomach’s sensitive because of anxiety, by all means spread out the food you eat over the course of the day instead of having large meals, just don’t…not eat. you will go into hypoglycemic shock and that will suck.

By the way, symptoms include:

Shakiness.

Nervousness or anxiety.

Sweating, chills and clamminess.

Irritability or impatience.

Confusion, including delirium.

Rapid/fast heartbeat.

Lightheadedness or dizziness.

Hunger and nausea.

(because of the nausea, eating might not feel like the thing to do at first. I’d suggest drinking a coke or something.)

I’ve dealt with sugar crashes before and I’ve collapsed and whited out. I’ve had friends do it too. If you think you’re going into hypoglycemic shock, and if there’s anyone else near by, tell them you think it’s happening, even if you’re not prone or it’s never happened before. If your’e alone, make your way slowly to the kitchen/wherever you have food/drinks. The standard rule is to take in 15 oz of a sugary drink (orange juice and soda–not diet–are the best) and wait 15 minutes to see if it’s over, then keep doing that until your sugar is stabilized. Then you can eat. If you think you’re about to collapse, especially if you start to feel dizzy, sit down and lay down or lean against something. Don’t risk injury, it’s better to pass out while you’re laying down than it is to collapse and hurt yourself.

*points at this more educated person*

If you are having trouble eating please keep in mind the BRATY diet. Bananas, Rice, Apple sauce, Toast, and (sometimes) Yogurt. These foods have been shown to be harder to throw up. By no means should this be the primary diet, but this can assist in the between times when it’s harder to keep things down.

this was really helpful

As someone who has a super nervous stomach this is super useful!!

I get this all the time at work particularly, good to know!

please please please teach your children to cook while they still live under your roof. even the most elementary things can’t be overlooked. because i just had to show my 24 year old boyfriend how to use a potato peeler and now i need to lay down for an hour

And for ppl who still need to learn and want to learn to cook, check out and subscribe to Brothers Green Eats on youtube. They have everything from how to legit cook everything from off the Wendys menu, off the Taco Bell menu, and off the Chinese food restaurant menu, to all the essentials you’ll need to have in your pantry and in your kitchen, to how to cook on a budget for a week and how to cook for a whole party worth of friends for understanding $10 and $20 – you’ll def be on your Chef Ramsay in no time after fucking with their channel!

Okay, everybody, I don’t talk much on here but this is important and I can’t find any other posts about it here.

There’s a little app called Be My Eyes. It’s been on iPhone for a while now and on October 5th, it’ll be out for Android too.

What is Be My Eyes, you might wonder? Well, it’s a community of people helping people. Namely, sighted people helping blind people with simple tasks that require sight to be simple.

See the picture?

(for those who can’t see, the picture shows the app I’m action. It shows a phone camera pointed at two red cans of food. Text above depicts a sighted person explaining the right can is a can of tamatoes.)

In short, if you’re blind and have every had trouble finding your blue shirt, the app was made for you.

If your sighted and want to help, the app is for you too.

If you’re not, reblog and spread this so more people can see.

can randomly generate just about ANYTHING. awesome for dms

Tabletop Audio: background music and sound effects for the ambience.

PCGen – a character creation program that handles all the tricky and tedious parts of building characters, including NPCs.

d20pfsrd.com – all the free information you would ever need to play Pathfinder, an alternative to D&D

DiceCloud: Interactive character sheet that can be edit and shared with yourself or others easily. Pulled up anywhere with internet connection on PC, Mac, or mobile device. Use it to also mark down health, death saving throws, spell slots, experience, and more on the fly.

DnDMagic: List all spells currently available from Player’s Handbook and Elemental Evil.

5th Edition Spellbook app: Make spellbooks for all your characters, manage spells, prepare spells. Keep track of Spell Save DC, and Spell Attack bonus on your mobile device.

Squire – Another character creation and management app. Contains most of the basic info and spells already, with options to create spells, items, classes/subclasses, etc. This is the free version, but pro has more options for DMs, including initiative order control.